|

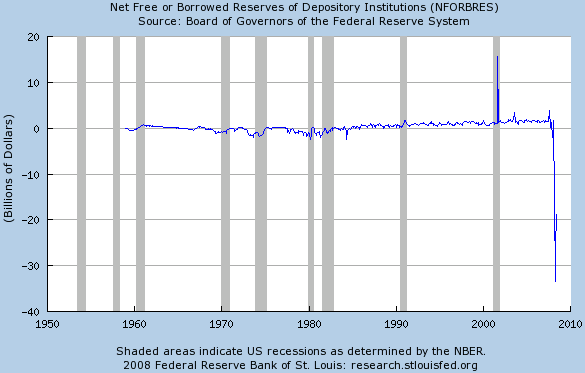

Borrowing AmericaInstead of building its full faith and credit, the United States government is becoming increasingly faithless and is losing credit by the second while sucking individual Americans into ever-greater debt. Yet, against all expectations, Americans seem to be waking up Wealth cannot be borrowed. For some not-so-unknown reason, Americans seem oblivious of that fact. The reason: they have been conditioned to view debt as ‘money’ for decades on end, while TV commercials showed them since childhood that all you need for the good life is a credit card from so-and-so bank – and a golden one, at that. As Peter Schiff noted in his recent article, by getting involved in the housing market, the government achieved the opposite from its stated end of making housing 'more affordable.' Because of cheap credit and lax lending, housing prices have doubled and tripled in some areas, while former homeowners were turned back into home-borrowers by being lured into taking out 'cheap' home-equity loans. Now, the money is gone and the bank owns their house. Hungry for RiskRates were so low that saving became impossible, turning appetite for risk (which is normal for the well-heeled and well-invested) into a depraved, ravenous hunger for higher returns shared even by ordinary retail savers. That, in turn, fueled the hedge-fund boom and the enron-ization of the US real-estate market. All of this has resulted in record-high mortgage default rates, which tumbled the entire pyramided-loan mess down the hillside and over the cliff. Major banks are threatening failure, and the government (aka Hank Paulson aka South Park’s ‘Mr. Hanky’) wants to subsidize their failure with endless taxpayer dollars. George Bush should have left Mr. Hanky floating in the Goldman-sewer. The following St. Louis Fed chart, showing the entire US banking system’s reserve position in historically ultra-deep hock, has been making the rounds, lately, but it is still instructive:

It’s pure poetry in motion - or poetic justice in action, rather. The banks that suckered well-meaning (but under-informed and therefore complicit!) Americans into the debt sewer are now deeply in hock themselves. Remember that 'reserves' are the foundation onto which banks must pyramid their loans. Reserves are composed of the banks' assets that exceed their liabilities. A percentage of those is supposed to be kept on account with the Fed. What does it all mean? The nation's banks have lost their asse(t)s in this bank-designed debt crisis, and now they have to borrow the difference. Ha! ‘Pimping’ OilIn the meantime, venerable brokerage houses like Goldman Sucks have perfected the neat little game of selling their investor-clients CDO’s, ABS’s, and interests in SIV’s while shorting the very same vehicles behind their customers' backs. Goldman, of course, the ever-present wheeler and dealer, also had its hands deep in the creation of the unsupervised (by the US government) ICE or "Inter-Continental Exchange" where they pimped, uhhm, pumped oil futures over the counter in ways that inevitably led to exorbitantly rising prices. Rumor has it that they and other investment houses also crammed huge oil tanks into large warehouses and filled them up with the real deal, ready for resale when the price would be high enough and which, atan opportune moment, could be sold into the market at a nice profit – and maybe for some additional benefits. That opportunity recently came when IndyMac went under and Fannie Mae and another "Mac" named Freddie threatened to follow suit. Both the dollar and the Dow were seriously taking on water while ripples of fear spread throughout the world financial system as it was faced with a potential US financial meltdown. The Fed was(is) dead in the water, rendered ineffective by its dual mandate of high employment and low inflation in the face of falling asset prices and rising consumer prices. Neither raising nor lowering the federal funds rate would have yielded any benefits – at least none that would have outweighed the dangers associated with each: cut the rate, lose the dollar, raise the rate, lose the Dow. Oil As a Policy Tool?So, the investment bankers' stashes of oil and their futures/options induced lock on oil price augmentation was used as a last-ditch policy tool by the establishment. When the dollar and the Dow tank and even the usual gold suppression doesn’t keep people in US stocks and treasuries, what's a banker to do? Well, sell oil, of course! That immediately helps the dollar recover and it gives people hope that 'the worst is over' in the recent oil spike, so they relax and maybe buy back into paper assets and start believing the financial press again. At the same time, fund manager money flows back out of gold and silver, which helps as well, and which can then easily be accelerated by some additional short selling from the cartel. Delivery problems? Bah, who cares? Fund managers don't want gold. Contracts are just fine. Problem solved. Naturally, I have not a shred of evidence that this is what really happened. I just follow my tried and true strategy of assuming the worst when it comes to how low the financial establishment will stoop in keeping their economic charade going for a little longer and in sticking it to even more to the asleep-at-the-wheel US investors and taxpayers. Combine that motive with power and opportunity, and you usually have a sure-fire bet that you're dead-on with your assessment. Yet, there may be evidence that Americans aren’t quite so dumb anymore. Are Americans Wising Up?There is one indication that they are, even though it looks like a measure taken in desperation, but then again, what’s wrong with a little desperation when you’ve had it way too good and way too easy for way too long? That resulted in a mental laziness that would lure Americans into letting their government get away with murder while they spent their kids’ inheritances and lived on phony, borrowed wealth. I am talking about a huge, surprising spike in the US personal savings rate as a percentage of disposable income. I know, that may not mean all that much at this point because incomes aren’t rising – while consumer prices are, often leaving precious little income to be disposed of in the process). Here is the chart:

That spike, achieved during the month of May alone, brought personal savings all the way back up to the level of 1995 – thirteen years ago! Of course, keep in mind that we are talking about savings as a percentage of an endangered and dwindling resource: disposable income. Looked at from that angle, at least theoretically, this chart can quite possibly be interpreted as nothing more than evidence of a huge spike in price inflation that yanked up the percentage of savings by the mere fact that disposable income is going zero-bound or even negative. Who knows? Naturally, the government (Bureau of Economic Analysis) has (supposedly real) disposable income growing in 2008. Amazing. With dwindling employment numbers and rising prices all around, Americans somehow managed to increase their disposable income. What a feat! How? Maybe when they default on their mortgages, they can now use all that free money for "disposal" purposes? Or, maybe the dollar has become so worthless in their eyes that they dispose of it by simply flushing it down the toilet. Anyway, here is some more evidence that formerly dormant synapses are beginning to fire again. Shaking the Shackles of (Treasury) Bondage?This following chart shows a very healthy (for Americans, not for the system) trend emerging. American investors don’t seem to be buying onto the Treasury bondage game quite as much anymore. It looks like the usual stocks-bonds Yoyo just went kaput this year.

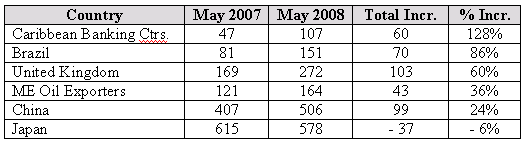

In a ‘healthy’ economy (where investors don’t think for themselves quite so much), investors who take money out of the stock market put it right back into the system by buying into the government bond market, and vice versa. That now doesn’t seem to be happening anymore, at least for the moment. Treasuries are in a downward trend even though the top foreign purchasers have dramatically stepped up their buying, against all expectations. Here is a table showing the year-over year change in Treasury holdings by the top foreign countries according to the Treasury's TIC data for May 2007-2008:

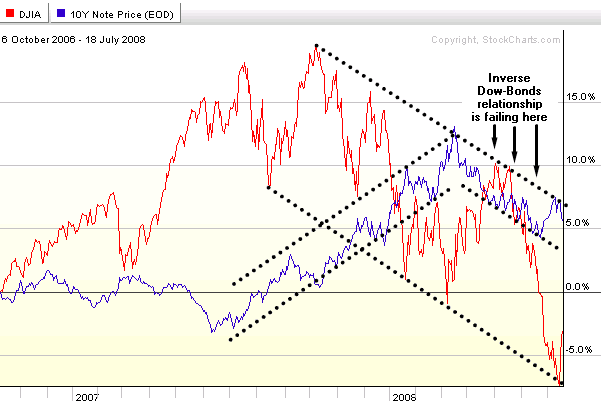

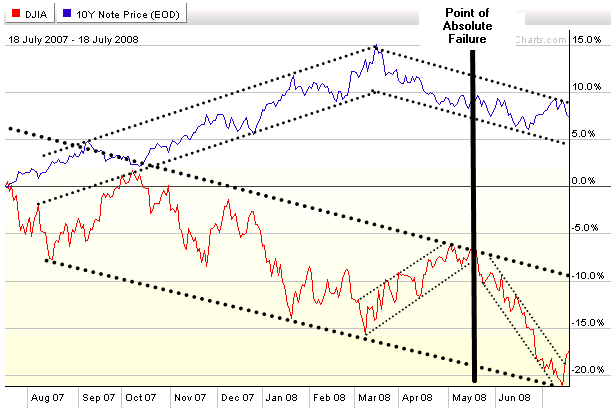

So, if the top holders have stepped up their buying, why are treasury prices falling? There is only one explanation: Americans aren’t buying into the scam anymore. They know that, in five ten, or thirty years, they won’t get back anything that has anywhere near the buying power of even today’s emaciated dollar. Here is another look at the Dow-10 Year Note comparison chart above, from a closer point of view, time wise:

On this chart, the fat vertical line is labeled “point of absolute failure” because that is the point in time when the normal closed-circuit system between stocks and bonds has stopped working, even on a short-term basis. The larger trend lines for the Dow, for example, include intermediate up and down movements during which the old Yoyo relationship has still been working before that point, i.e., from March 11th, when the Dow bounced until mid May, the point of absolute failure). Since then, however, the downtrend in ten-year T-Note prices has continued right alongside the narrow intermediate-term downtrend channel of the Dow. That’s scary stuff for the guardians of this closed circuit investment loop. It means money is escaping their system, and that’s bad for them. Where Does All the Money Go?It may go to foreign stocks, bonds, or gold and silver and their producer stocks. Foreign stock markets have been taking on water just like the American ones, though, with the few notable exceptions of the Brazilian BOVESPA and maybe Saudi stock markets. Foreign bond markets are more interesting in that respect because there are some fairly high-yielding currencies out there, like the Australian dollar, for example, which at 7.25% yields more than three times what the dollar yields, or the euro, the yield of which is twice that of the dollar. Yet, all of these currencies are falling against gold – so where would you want to put your money? And that’s exactly what more and more people (and even fund managers) are starting to think. It is also the only point of safety for anyone who doesn’t want to spend their retirement in one of those luscious, luxurious tent cities springing up near major metropolitan centers around the country these days. Wrap UpTo wrap it all up, the enormous spike in the personal savings rate seems to indicate Americans are saving more than they used to. That maybe bad news for the economy, which needs them to spend, and the banks, which need them to borrow, but it is definitely good news for Americans individually because a ‘good economy’ or rich bankers don’t really help you very much when you’re deep in debt and out of a job. Taking care of number one makes more sense, and it is even good for the economy in the longer run. It also looks like Americans are staying off their government's bond market, which will keep them in good shape years down the road. Now, if they could only make the final leap of logic that dictates investing in the one thing compared to which most other assets are destined to fall in the long run – gold and silver – then there may actually be some hope that Americans might stop trying to borrow the American dream - and start living in economic reality again. We’ll have to wait and see how all this turns out. Got gold? Alex Wallenwein |